Investing in buy-to-let property in the UK can be a lucrative venture. However, it’s essential to understand the various taxes involved to ensure compliance with the law and optimize your returns.

This article provides an overview of the key taxes you should be aware of when investing in UK buy-to-let property and how you can keep on top of them.

This buy to let guide from RWInvest can offer further information too – remember, everyone’s financial goals differ so think about what will work best for you.

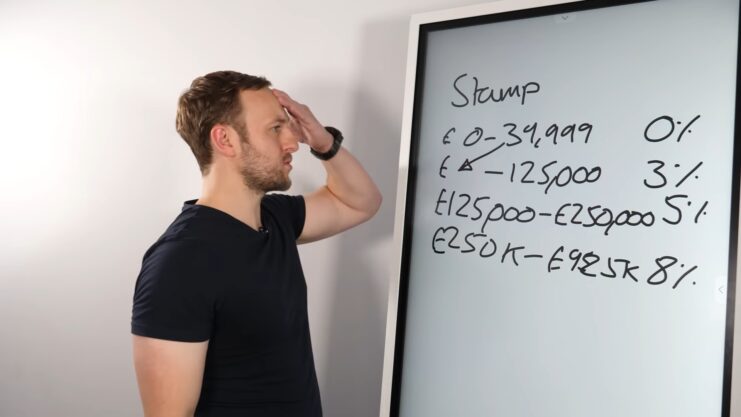

Stamp Duty Land Tax (SDLT)

When purchasing a property in the UK, you may be liable to pay Stamp Duty Land Tax. The amount depends on the property’s value and whether you already own another property. As of June 2024, the rates for residential property purchases are as follows:

- Up to £250,000 Zero

- The next £675,000 (the portion from £250,001 to £925,000) 5%

- The next £575,000 (the portion from £925,001 to £1.5 million) 10%

- The remaining amount (the portion above £1.5 million) 12%

Income Tax

Rental income generated from buy-to-let properties is subject to income tax. The tax is calculated based on the rental profits after deducting allowable expenses.

These expenses may include mortgage interest (phased out for higher-rate taxpayers), property maintenance costs, letting agent fees, and insurance premiums. The income tax rates for rental profits are:

- Basic rate taxpayers: 20%

- Higher rate taxpayers: 40%

- Additional rate taxpayers: 45%

Capital Gains Tax (CGT)

When you sell a buy-to-let property, any capital gains realized may be subject to Capital Gains Tax. The taxable gain is calculated as the difference between the sale price and the property’s acquisition cost, after deducting allowable expenses and any capital improvements.

The current rates for CGT are:

- Basic rate taxpayers: 10%

- Higher rate and additional rate taxpayers: 20% There is also a tax-free allowance called the Annual Exempt Amount (£12,300 for the tax year 2022/2023). Special rules may apply for non-residents.

Inheritance Tax (IHT)

Upon your passing, the value of your UK buy-to-let property may be subject to Inheritance Tax. The standard IHT rate is 40%, but there is an initial tax-free threshold of £325,000 (known as the Nil Rate Band). Additional allowances and exemptions may apply, such as the Residence Nil Rate Band for main residences left to direct descendants.

Additional Taxes:

- Council Tax: As the property owner, you are responsible for paying council tax unless it is included in the rental agreement and paid by the tenant. b.

- Annual Tax on Enveloped Dwellings (ATED): If you hold the property in a corporate envelope, ATED may be applicable. The rates vary based on the property value and ownership structure.

- Value Added Tax (VAT): VAT may be applicable if you purchase a new-build property or opt to tax a commercial property for rental purposes. Seek professional advice to determine the VAT implications.

Mortgage Interest Relief Changes

It is essential to note that the UK government has been phasing out mortgage interest relief for buy-to-let properties. By the current tax year, the deduction for mortgage interest is limited to the basic rate of income tax (20%).

Seek Professional Advice

Tax regulations can be complex, and it is advisable to consult with a tax professional or accountant who specializes in property investment to ensure you comply with all tax requirements and identify any available tax reliefs or allowances.

Remember, tax laws and rates can change over time, so it is crucial to stay updated with the latest regulations.

Keep Accurate Records

Maintain organized and detailed records of all income and expenses related to your rental property. This includes rental income, mortgage interest payments, repairs and maintenance costs, insurance premiums, agent fees, and any other relevant expenditures. Accurate record-keeping will help you during tax filing and can also serve as evidence in case of an audit.

Claim Allowable Expenses

Familiarize yourself with the allowable expenses that can be deducted from your rental income. By maximizing your eligible deductions, you can reduce your taxable rental profits and potentially lower your overall tax liability. Keep receipts and documentation for all expenses to support your claims.

Consider Tax-efficient Ownership Structures

Depending on your financial circumstances and long-term goals, it may be beneficial to hold your buy-to-let property in a specific ownership structure. For example, forming a limited company could offer tax advantages, as mortgage interest relief changes do not apply to corporate entities. However, individual circumstances vary, so seek professional advice to determine the most suitable ownership structure for your situation.

Stay Updated with Regulatory Changes

Tax regulations and legislation can change over time, impacting the tax implications for buy-to-let investors. Stay informed about any updates or changes in tax laws through official government sources, tax publications, or by consulting with a tax professional. Being aware of changes allows you to make informed decisions and adapt your investment strategy accordingly.

Consider Tax Planning Strategies

Engage in proactive tax planning to optimize your tax position. This may involve utilizing tax allowances, timing property sales strategically to minimize CGT liability, considering gifting or trust arrangements for estate planning purposes, or exploring other tax-efficient investment options alongside buy-to-let properties.

Seek advice from a qualified tax professional to explore potential tax planning opportunities.

Stay Compliant with Reporting Obligations

Ensure you meet all reporting and filing obligations imposed by HM Revenue and Customs (HMRC). This includes registering for Self Assessment if required, submitting annual tax returns on time, and providing accurate and complete information. Failing to comply with reporting obligations can result in penalties and interest charges.

Remember, this guide provides general information and should not substitute personalized advice from a tax professional. Tax implications can vary depending on individual circumstances, so it’s crucial to seek professional guidance tailored to your specific situation and goals.